![[From the Loveland School District] November 2019 Levy FAQ](https://lovelandmagazine.com/wp-content/uploads/2019/08/feature-local-election-guide-b.jpg)

Loveland, Ohio – Below is a post from the Loveland City School District about the combined 16.78-mill levy that will be on the Fall ballot. At the bottom of this page, you will find levy information provided by Loveland Magazine.

Note: This resource will be updated with answers to additional commonly asked questions.

Helpful Resources

Directions for accessing the information from your county auditor can be found under “Calculating the Tax” on this website.

coming weeks, there will be several opportunities for community involvement through small and large group meetings. The current schedule is available here. You are also welcome to call the Superintendent, Dr. Amy Crouse, or the district Treasurer, Mr. Hawley, who welcome the opportunity to answer your questions on the urgency and necessity of this levy request.

coming weeks, there will be several opportunities for community involvement through small and large group meetings. The current schedule is available here. You are also welcome to call the Superintendent, Dr. Amy Crouse, or the district Treasurer, Mr. Hawley, who welcome the opportunity to answer your questions on the urgency and necessity of this levy request.Funding Questions

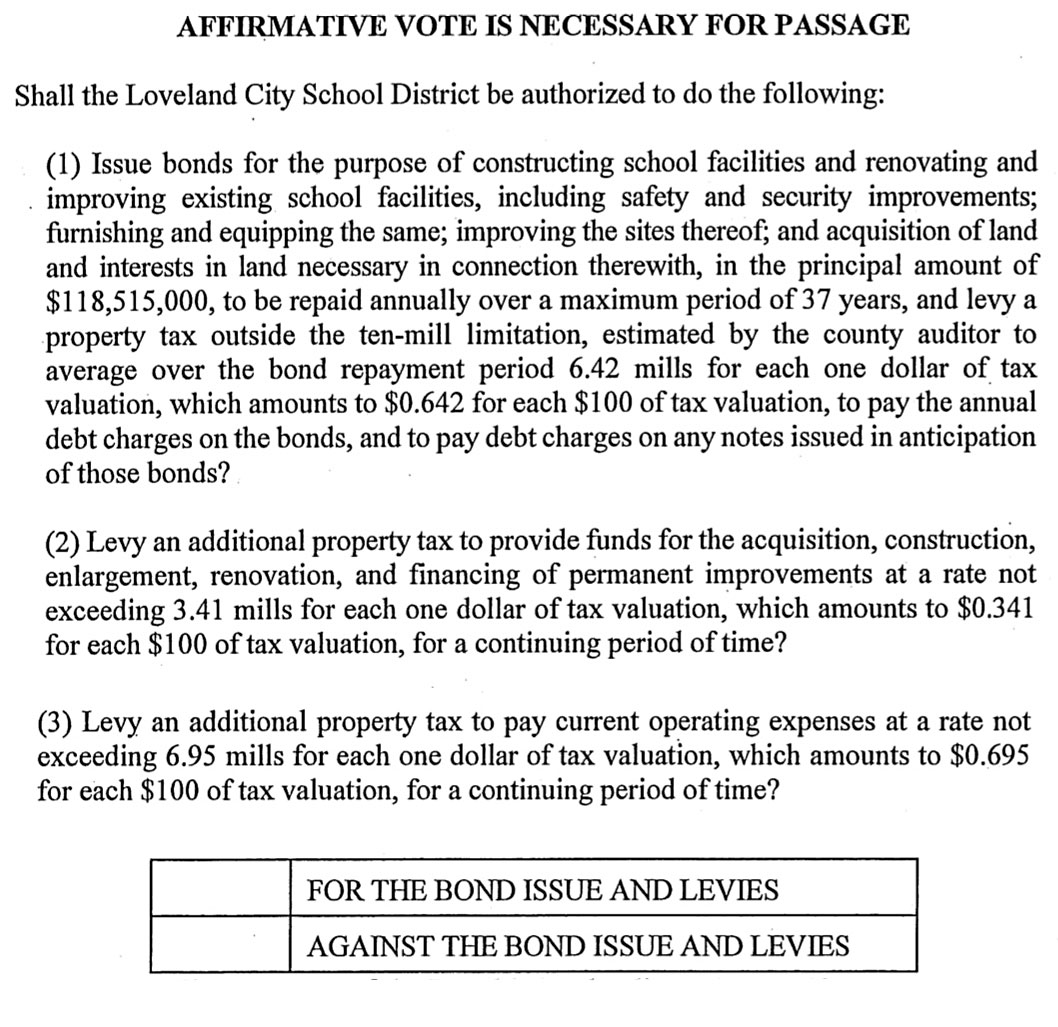

The November 5 request includes an operating levy, which is necessary with or without the building levy, to run the daily operations of the school district. The permanent improvement and bond portions of the levy are for the much-needed modernization, construction, repairs, and renovations that are outlined in the facility master plan.

![]() 2. What is an operating levy for?

2. What is an operating levy for?

An operating levy is used to provide money for a school district’s day-to-day operating expenses, including utilities, supplies, and salaries/benefits for staff. The November 2019 operating levy for Loveland Schools is a continuous levy. It will be collected each year, but as home values increase, the tax rate will be reduced in order to hold the payment to the schools at a constant level. This is often referred to as the “tax reduction factor,” or the “HB 920 reduction factor.” HB 920 is a state law that protects homeowners from paying more money in taxes as their homes appreciate.

This taxpayer protection means revenues remain flat for the schools during the life of the levy, but in the normal course of business, operating expenses rise due to inflation and increased educational requirements. This is the reason the schools typically must return to voters and ask for additional operating funds every three to five years.

The last operating levy for Loveland Schools was forecasted to cover four years of expenses, and the district has been able to sustain operations for five and a half years since approval.

3. What is a bond levy or bond issue?

The last bond issue for Loveland Schools was passed in 1998. It provided the funds to build the current intermediate school, renovate the middle school and add an auxiliary gym and large classroom at the high

school. The school buildings have been exceptionally well-maintained over the years, but two separate assessments, including one by the Ohio Facilities Construction Commission, show that the cost of maintaining the Early Childhood Center, Primary and Elementary Schools is more expensive than replacing them.

4. What is a permanent improvement (PI) levy for?

Like a bond levy, a permanent improvement levy (PI levy) can be used only for a certain category of needs. Per state law, funds from a PI levy can only be used for the purchase of items that have a lifespan of five years or more (a capital improvement), or to repay financings used to purchase or construct capital improvements. PI funds can be used for building construction, maintenance and repairs, and certain equipment that is designed to last at least five years. For example, they can be used to replace roofs, windows, and HVAC systems, etc. PI levies cannot be used to pay for salaries, benefits, operating expenses, or basic supplies.

5. What will the impact be on our property taxes?

The cost of the 16.78-mill combined operating and permanent improvement/bond levy translates into $587.30 annually or $49 monthly per $100,000 of appraised home value as determined by your local county auditor. For more details, please see the section “Calculating the Tax” on this page.

6. What is a “mill?”

For tax purposes, a home is taxed on its assessed value, not its appraised or market value. The assessed value is 35% of the appraised value as determined by the local county auditor. For example, a home that is appraised at $100,000 by the auditor is taxed only on $35,000.

8. Why is the Board of Education requesting this combined levy now rather than in phases?

The master plan was developed through extensive analysis with subject matter experts and community engagement over the past several years, including large community meetings, targeted focus groups, and a community-based finance committee, which concluded that the chosen plan is the most cost effective for residents. The district is able to take advantage of historically low interest rates at this time and the adopted master plan will be completed in the shortest timeframe possible, minimizing the disruption to students and instruction, as well as the impact of increasing cost of materials and construction over time.

9. Is there another way to generate the money needed other than using a property tax? For example, a sales tax or an income tax?

By law, a school district cannot levy a sales tax. The district evaluated alternatives, including an income tax, but the current plan as presented was determined to be the least costly to the greatest number of residents by a group of community member volunteers. This group worked on various funding options with the assistance of a taxation specialist retained by the Board of Education. The current plan provides the least costly option based on several primary factors: current low interest rates, anticipated (high) future inflation rates, and potentially expensive future unfunded state mandates.

10. How is the district financially accountable and how has it maintained the existing infrastructure?

The district consistently earns accolades for strong fiscal management and excellent record keeping. This includes a high bond rating from Moody’s of Aa2. The district has a solid history of only asking the voters for what it needs and then making additional adjustments to the budget to stretch the dollars. Only 32% of the district budget comes from the state and the remainder is locally-generated revenue. It has been five years since the district asked for operating dollars and at that time promised the taxpayers it would last four years. In addition, the only remaining bond issue in the district will be paid in full within the next five years.

The district operates on an ongoing five-year maintenance plan to ensure safety, provide for upkeep, and to extend the life of the buildings. As buildings age, however, they become increasingly more difficult and costly to maintain.

11. How does our per pupil spending compare to other similar districts?

11. How does our per pupil spending compare to other similar districts?

The state average for per-pupil spending is $11,953/year. As a fiscally conservative district, Loveland spends approximately $1,000 less, but allocates proportionally more to classroom instruction. Compared to other, similar school districts in the area, the district spends less than Mason, Forest Hills, Madeira, Wyoming, Mariemont, and $4,000 less per pupil than Sycamore and $5,000 less than Indian Hill.

12. What happens if the ballot issue fails?

The financial needs and the needs of the buildings in the district will not go away. The facility master plan outlines the repairs, renovations and additions that are needed today; the cost of meeting those needs will continue to increase over time. Without the necessary operating funds, the Board of Education would have to evaluate and execute budget cuts, which would have a direct impact on classroom instruction and the quality of education in the district.

Facility Master Plan Questions

1. What is the new property the school district is considering purchasing? Why is it needed and what are the plans for current properties?

1. What is the new property the school district is considering purchasing? Why is it needed and what are the plans for current properties?The Loveland Board of Education adopted a resolution at the March 19 business meeting to approve a contract for the option to purchase real estate in Clermont County. The approximately 110-acre large piece of land – part of a property known as Grailville – is currently owned by the Grail, an Ohio nonprofit organization. The Grail plans to maintain property on the opposite side of O’Bannonville Road.

For the first time in many years, Loveland Schools has the opportunity to purchase a large enough plot of land for a new campus. The current LPS/LES and LECC campuses are not large enough to allow for additions or to demolish and build new, based on state recommendations for the current (and projected) number of students at these locations. The district is looking into various options for the LECC and Loveland-Madeira campuses once vacated, but no decisions have been made, and cannot be made until a bond is passed.

![]() The current 1st-4th grade building is really two buildings in terms of square footage – the number of students requires two gyms, two cafeterias, two entrances, and two admin suites. Today, Loveland’s Pre-K through 5th grade students are spread across four different buildings on three campuses. The efficiency in the master plan is captured by sharing a campus. It is more efficient to maintain one versus multiple campuses. Very large elementary schools are undesirable for the learning and developmental needs of students, which is why the new master plan has three buildings (PK/K; 1st-2nd; 3rd-5th) on the Grailville site.

The current 1st-4th grade building is really two buildings in terms of square footage – the number of students requires two gyms, two cafeterias, two entrances, and two admin suites. Today, Loveland’s Pre-K through 5th grade students are spread across four different buildings on three campuses. The efficiency in the master plan is captured by sharing a campus. It is more efficient to maintain one versus multiple campuses. Very large elementary schools are undesirable for the learning and developmental needs of students, which is why the new master plan has three buildings (PK/K; 1st-2nd; 3rd-5th) on the Grailville site.

3. What will the impact of a new campus be on traffic?

3. What will the impact of a new campus be on traffic?

The district is in the early stages of working on possible bussing and routing alternatives. Preliminary mapping shows a reduction of trips through downtown Loveland and the opportunity to go in the opposite direction of “rush hour” traffic. The campus will be accessible from both O’Bannonville Road and Route 48/Oakland Road, and the property is large enough for improved staging for buses and parents. It will not be a high school campus, so student drivers will not be impacted by the plan. Currently, about 50 percent of the students are transported daily from Hamilton County to Clermont County (and vice versa) for school, which will not change by adding the new campus.

Once a bond is passed, approximately a year of designing the campus and at least another year of construction will follow. Students will not move into new buildings until the fall of 2022 at the earliest, which provides ample time to seek positive solutions for safe transportation. The district continues to have a strong relationship with the City of Loveland and Miami Township and will work with them to accomplish a mutually agreeable plan for bussing and routing.

4. What does the phasing/timing of the master plan look like? Isn’t the plan just a “wish list?”

4. What does the phasing/timing of the master plan look like? Isn’t the plan just a “wish list?” - Addresses the space and facility needs identified in two separate assessments.

- Can be completed in the shortest amount of time, limiting disruption to students and staff and minimizing costs that increase over time.

- Provides for the safety of students and staff.

- Captures the input of community, staff, and students.

- Allows for additional programming; supports instruction for students that will allow them to compete in the 21st century workforce; and maintains the momentum in academic improvements at Loveland.

Key components of the plan:

- Provides new buildings for Pre-K – 5th grade.

- Provides a building addition, as well as repairs, renovations and enhancements to the high school.

- Provides repairs, renovations and enhancements to the middle school.

The district has reached out to several groups/corporations that have successfully partnered with other districts in the area. In these arrangements, the district is typically required to fund the development

of land or facility space. Once built, however, the third-party partners could manage the facility and share operating costs or other gain-share arrangements. Such partnerships may benefit the school district later, but the upfront cost of construction increases.

The district has identified corporate partners that are willing to provide lab equipment and furnishings for specific programming in the new facilities. In addition, it is possible that the Loveland City School District would provide a small amount of square footage at the Pre-K – 5th grade campus to a partner to operate a health clinic that would be accessible to students, families, and the community.

The master plan does not include a community center, pool or other community facility at this time, but the district is open to discussions on future use of the properties that will be vacated per the master plan. Discussion will continue with other parties and entities, including the City of Loveland, who are interested in collaboration on what type of use would best serve the community.

The next meetings of the Board of Education are:

September 3 – Board work sessions are held on the first Tuesday of the month at 6 p.m. in the Board of Education administrative offices.

To contact Board members:

President, Art Jarvis jarvisar@lovelandschools.org

Vice President, Kathryn Lorenz, Ph.D. lorenzka@lovelandschools.org

Member, Michele Pettit pettitmi@lovelandschools.org

Member, Ned Portune portunne@lovelandschools.org

Member, Eileen Washburn washbuei@lovelandschools.org

To contact the Administration

Superintendent Dr. Amy Crouse (513) 683-5600 crouseam@lovelandschools.org

Treasurer/CFO Kevin Hawley (513) 683-5600 treasurer@lovelandschools.org

Read: Grailville and School District Option to Purchase Agreement and Appraisal

Loveland Magazine “Local Voter Guide” to issues and candidates

![]()