WASHINGTON — Taxpayers across the United States could be guaranteed a free public option to file federal tax returns online as the Internal Revenue Service announced plans Thursday to make its Direct File program permanent.

The pilot program offered in 12 states from March to April drew roughly 140,000 accepted returns this filing season and saved participants $5.6 million in tax preparation costs and helped filers receive $90 million in refunds, according to the IRS.

The states involved in this year’s pilot included Arizona, California, Florida, Massachusetts, Nevada, New Hampshire, New York, South Dakota, Tennessee, Texas, Washington and Wyoming.

The agency is now inviting all 50 states to participate and will accommodate however many sign on, Treasury Secretary Janet Yellen and IRS Commissioner Danny Werfel told reporters on a call Thursday morning.

“We heard directly from hundreds of organizations across the country, more than 100 members of Congress, individual direct file users and those that are interested in using direct file. The clear message is that many taxpayers across the nation want the IRS to provide options for filing electronically at no cost,” Werfel said.

Yellen touted results of a user survey that showed 90% of participants rate their experience as excellent or above average.

“They appreciated that it allowed them to quickly fix mistakes and there were no fees or upsells. The success of the Direct File pilot means there’s now strong demand for direct file from taxpayers across the country,” Yellen said.

The average American spends $270 and 13 hours filing their taxes, according to the agency’s Taxpayer Burden Survey.

The program ‘delivered’

The left-leaning Economic Security Project, which advocates for tax credits for low-income and middle class households, praised the IRS decision to make permanent the program that “delivered on the promise of free and simplified tax filing for taxpayers.”

“It was evident that taxpayers saw the value of Direct File, both in making their lives easier and demonstrating what great government customer service looks like,” Adam Ruben, the organization’s vice president of campaigns and political strategy, said in a statement Thursday.

“We are already working with our partners in states across the nation to support the expansion of Direct File next year so more taxpayers can take advantage of free and simplified tax filing in the next tax season,” he said.

Democratic Sen. Ron Wyden of Oregon, the top tax writer of the upper chamber, praised the IRS announcement in a statement Thursday as “tremendous news for taxpayers all over the country who are tired of getting ripped off by the big tax prep companies that routinely upcharge for unnecessary services, oversell the quality of their products and offer crummy customer service.”

Werfel said the IRS cannot provide an estimated cost of expanding the program because the agency has yet to learn how many states will jump on board.

The cost to run the program this year totaled $31.8 million, breaking down to $24.6 million in IRS costs, and $7.2 million in U.S. Digital Service costs to create the online platform, Werfel said.

Among the tens of billions of dollars Congress authorized for the IRS in its 2022 budget reconciliation law, otherwise known as the Inflation Reduction Act, $15 million was earmarked for exploring a way for the public to electronically file federal returns for free directly to the government, rather than through a third party.

This year’s pilot program was only available to taxpayers with basic tax situations, including W-2 income or simple credits and deductions, like the child tax credit or student loan interest.

“Our goal is to gradually expand the scope of Direct File to support most common tax situations, focusing in particular on tax situations that impact working families,” Werfel said.

When asked on the call whether the success of the program depends on who is in the Oval Office next year, Werfel responded, “I truly believe that the vision that the IRS has for the future tax administration is a nonpartisan one.”

Opposition from GOP

The free public program was met with fierce opposition from congressional Republicans and GOP state officials who criticized it as redundant, “unconstitutional” and a threat to state tax revenue.

Many cited the already established IRS Free File program, a regularly evolving partnership between the federal agency and private tax prep software companies that provide a free federal return filing option.

That 22-year-old program has been riddled with issues, including low participation and “confusion and complexity” that led millions of eligible taxpayers to actually pay the commercial partners who were supposed to offer the free service, according to a 2019 Treasury Inspector General for Tax Administration report.

A 2019 ProPublica investigation revealed deliberate tactics by Free File participant Intuit, maker of TurboTax, to cloud access to the free option.

Nearly two dozen state auditors, comptrollers and treasurers from 18 states urged the IRS to “shut down” the new Direct File pilot program because users could be confused about having to file a state return separately, therefore resulting in a loss in state revenue.

This argument is based on the fact that many commercial tax prep software companies and private tax preparers automatically prompt taxpayers to complete their state returns after filing the federal one.

The state officials who signed on to the March 25 letter to the IRS hailed from Alaska, Florida, Idaho, Indiana, Iowa, Kansas, Kentucky, Louisiana, Mississippi, Nebraska, North Carolina, Ohio, Oklahoma, South Carolina, South Dakota, Utah, West Virginia and Wyoming.

Two of the Direct File pilot program states — Arizona and New York — worked with the nonprofit Code for America to integrate a free state tax return filing option in concert with Direct File. The nonprofit reported that of the state returns filed through its tool, 98% were accepted.

Several state governments already offer free public electronic filing for state income tax returns that users must access separately through dedicated state websites, including Alabama, Kansas, Kentucky and Pennsylvania, which offer the service regardless of income level. Some states, like California and Iowa, have income thresholds for free filing.

![[Meeting Videos] Christman Farm sale moves forward after public hearing](https://lovelandmagazine.com/wp-content/uploads/2020/10/feature-HOMEARAMA-1.jpg)

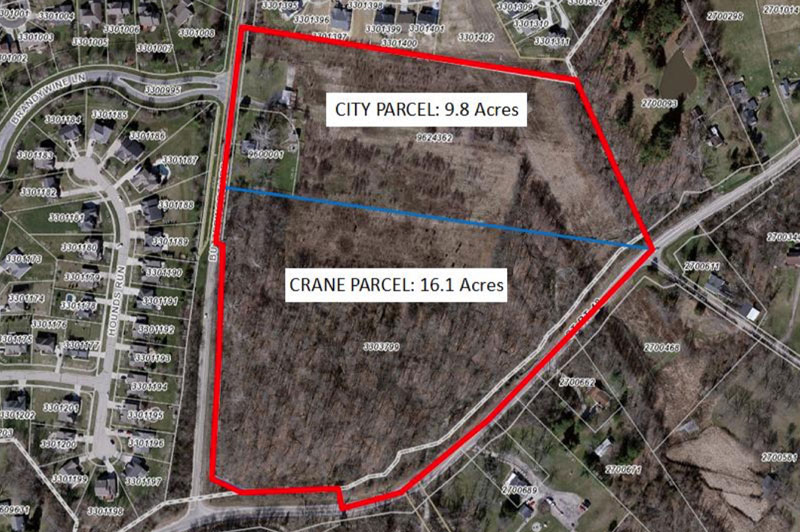

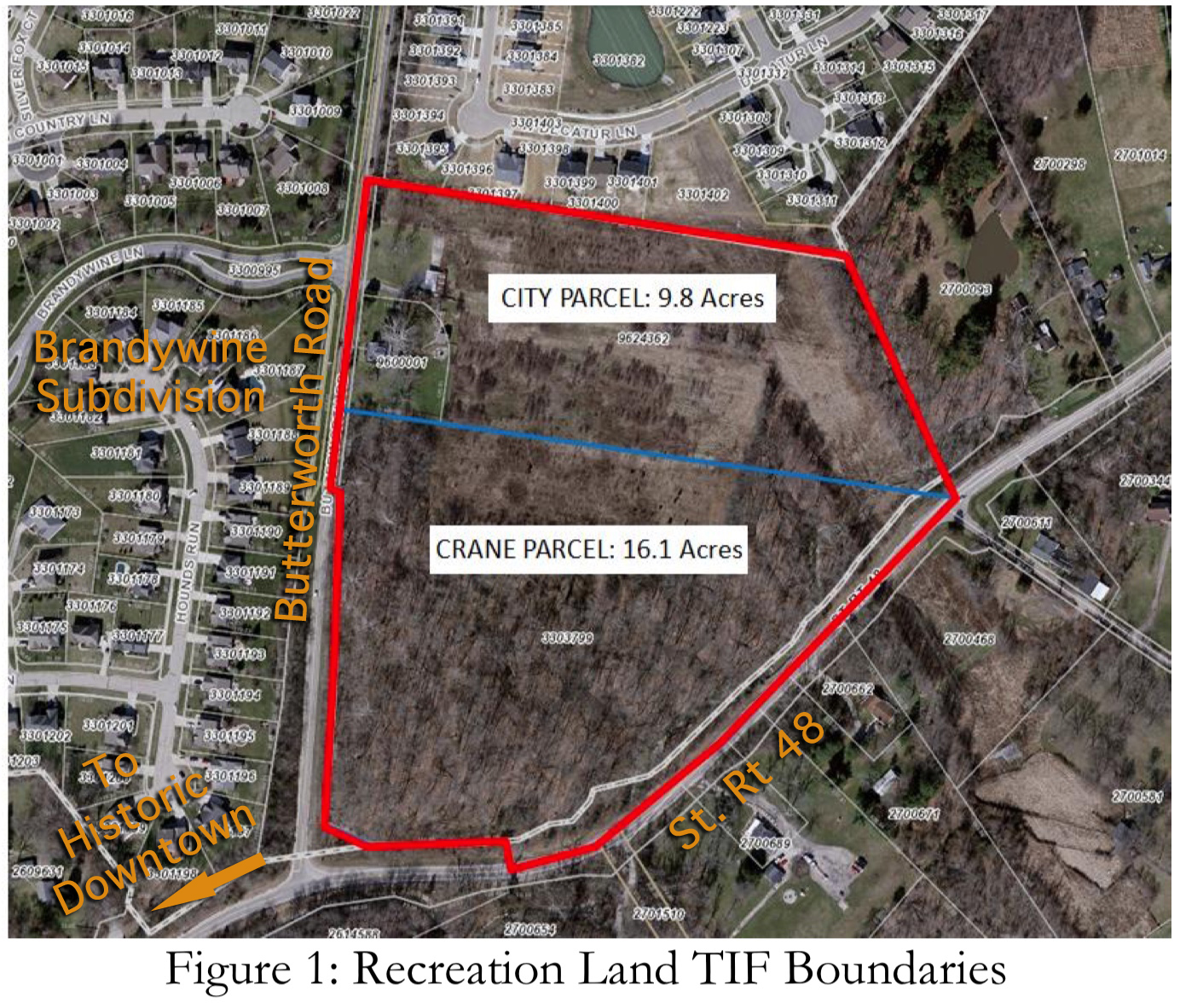

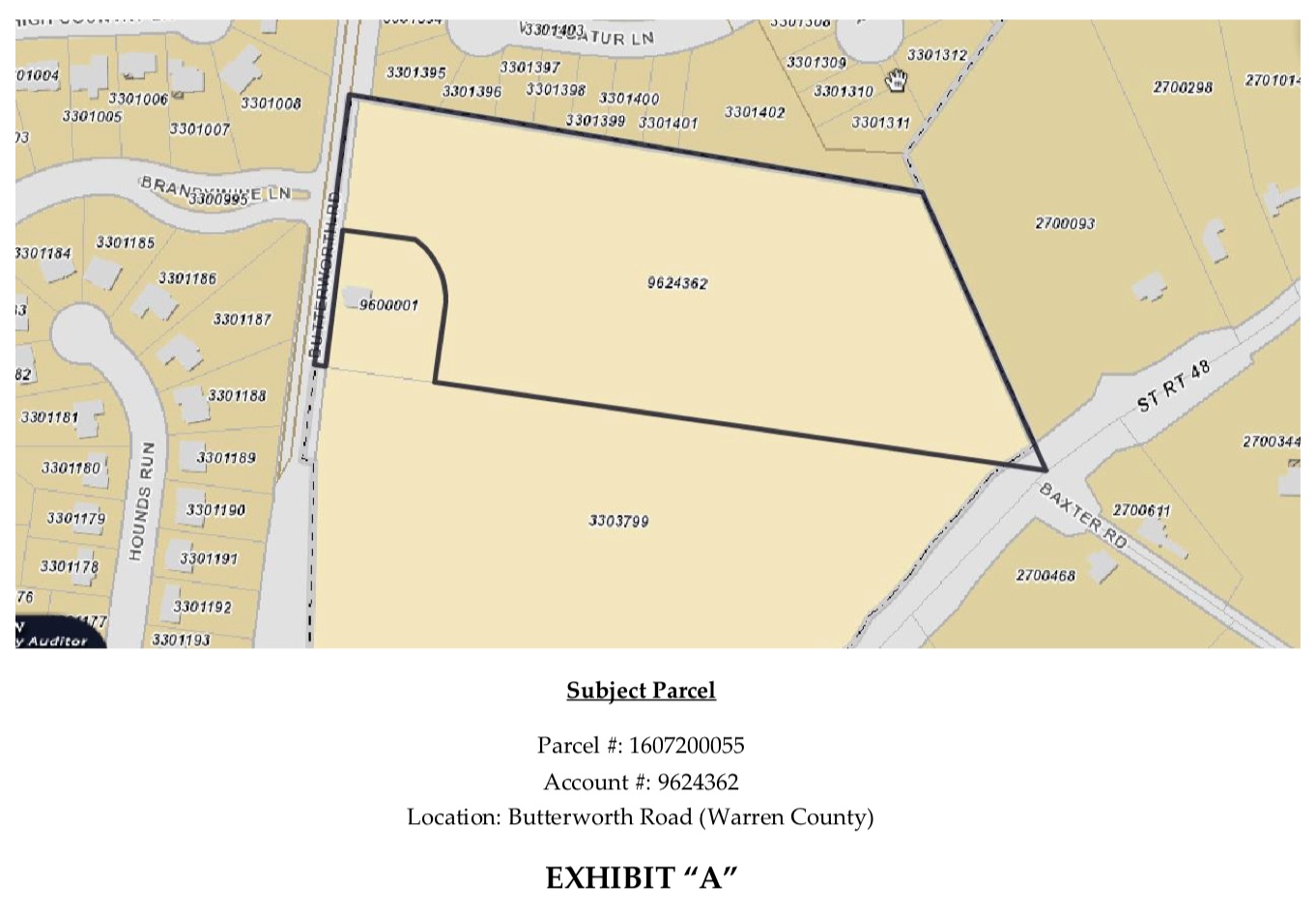

A Recreation Tax Increment Financing District (TIF) was created by Ordinance 2008-38 to pay off the financing. The TIF consists of approximately 27 acres and includes the taxpayer-owned property known generally as the Christman Farm as well as the Crane property which is privately owned.

A Recreation Tax Increment Financing District (TIF) was created by Ordinance 2008-38 to pay off the financing. The TIF consists of approximately 27 acres and includes the taxpayer-owned property known generally as the Christman Farm as well as the Crane property which is privately owned. Campbell Berling is proposing that future homeowners be allowed to pay the cost of sewer line extensions over 20-years.

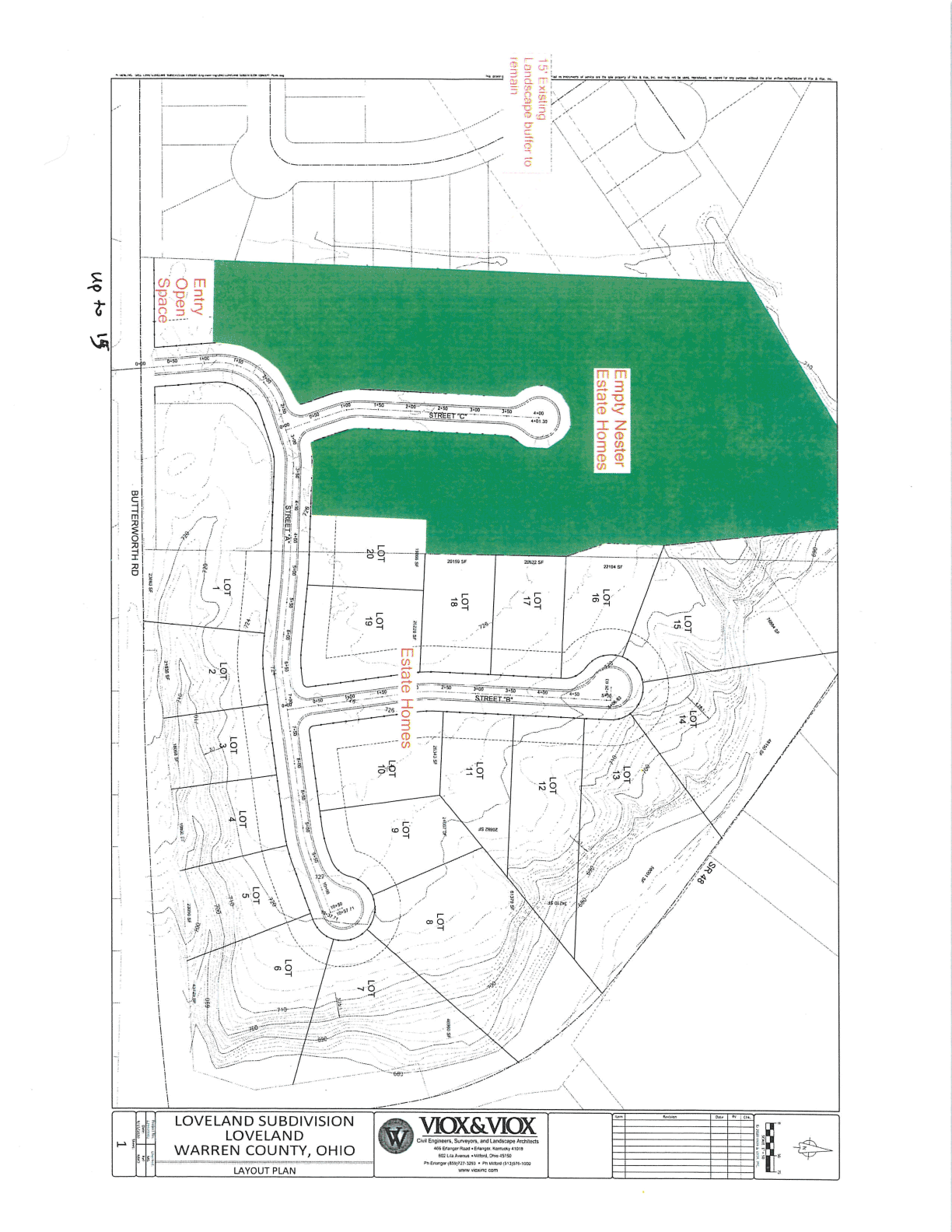

Campbell Berling is proposing that future homeowners be allowed to pay the cost of sewer line extensions over 20-years.

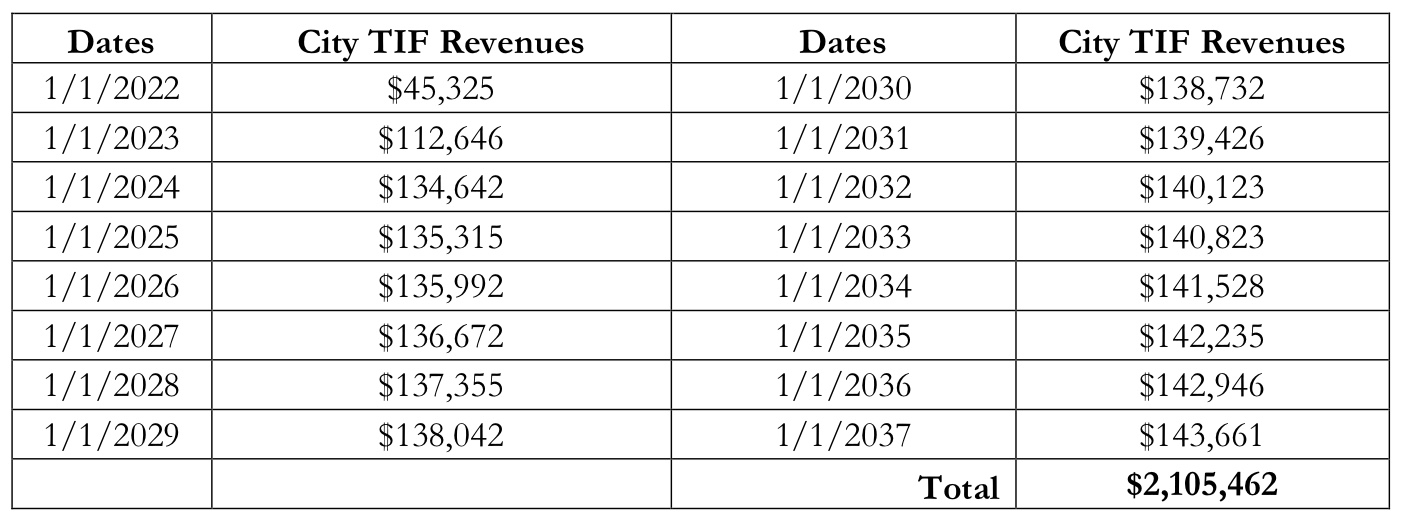

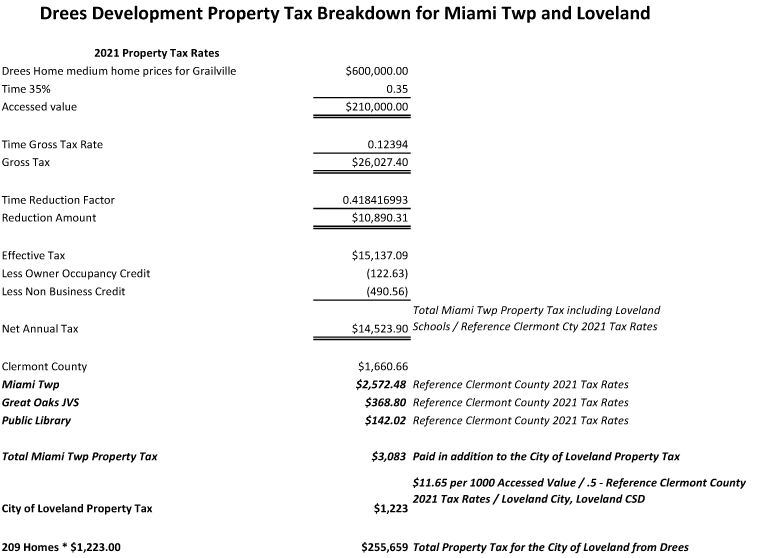

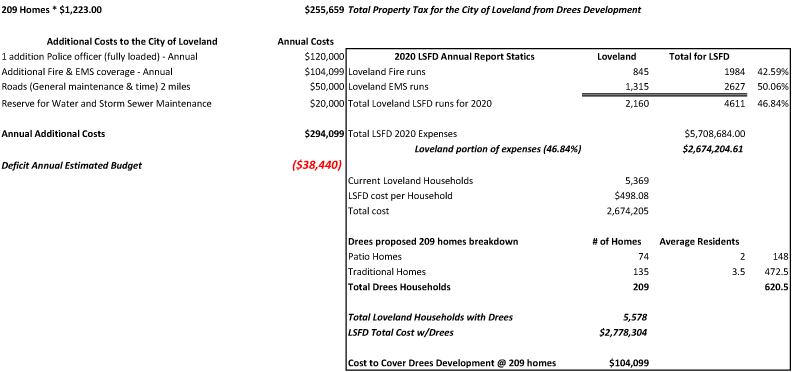

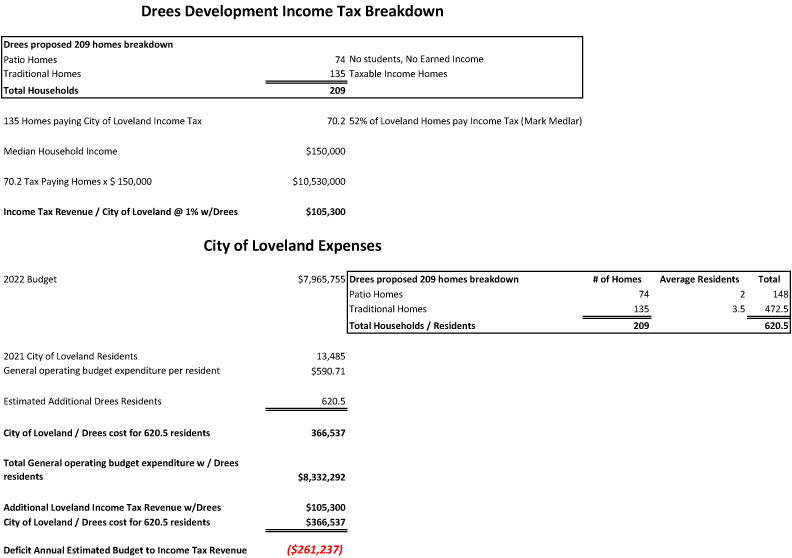

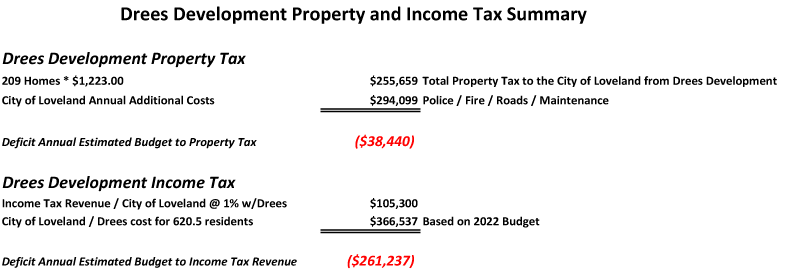

Kennedy presented this “Fiscal Impact” study in the package of information he presented to City Council:

Kennedy presented this “Fiscal Impact” study in the package of information he presented to City Council:

Taxpayers originally bought

Taxpayers originally bought

Campbell Berling is proposing that future homeowners be allowed to pay the cost of sewer line extensions over 20-years.

Campbell Berling is proposing that future homeowners be allowed to pay the cost of sewer line extensions over 20-years. Kennedy presented this “

Kennedy presented this “